No Retirement Corpus is safe.There are only probabilities

- Riddhi Dhariwal

- May 14

- 3 min read

Updated: May 15

Retirement planning has become one of the defining financial anxieties of the Indian middle class. Unlike previous generations that often relied on pensions from government employment, a large section of today’s workforce must self-fund retirement over increasingly long lifespans.

Unfortunately, retirement planning discussions are often reduced to simplistic rules of thumb or excessively conservative targets that are counterproductive.

In this article, we demystify retirement planning and discuss interesting trade-offs.

Problem Statement

Following the work of Bengen1 and the subsequent Trinity study2, modern retirement planning is usually formulated as follows:

Q: What is the minimum starting retirement corpus required to sustain constant-inflation-adjusted withdrawals over a retirement horizon of N years?

For the purposes of this analysis, we utilize a baseline persona reflecting the modern Indian professional:

Current Age: 35 (Retiring at 60)

Retirement Duration: 30 years

Annual Expenses (Present Value): ₹24 Lakhs (₹2 Lakhs/month)

Assumed Inflation: 6%

The retiree withdraws inflation-adjusted spending every year to preserve purchasing power.

The second output of the optimization problem is the asset allocation between equity and debt.

Certainty - the destroyer of wealth

There are hidden assumptions in the question. Nothing in life is certain - in investing even less so. Hence there is no safe corpus.

So we use a different metric - certainty of not running out of money in retirement.

Usual published research works with Certainty = 95%. The corpus and asset allocation are then computed using Monte Carlo simulations3.

However, as with most things in life, high certainty comes at a high cost.

In investing, this tradeoff appears between fixed deposits and equities.In careers, it appears between stable employment and entrepreneurial upside.

Retirement planning is no different.

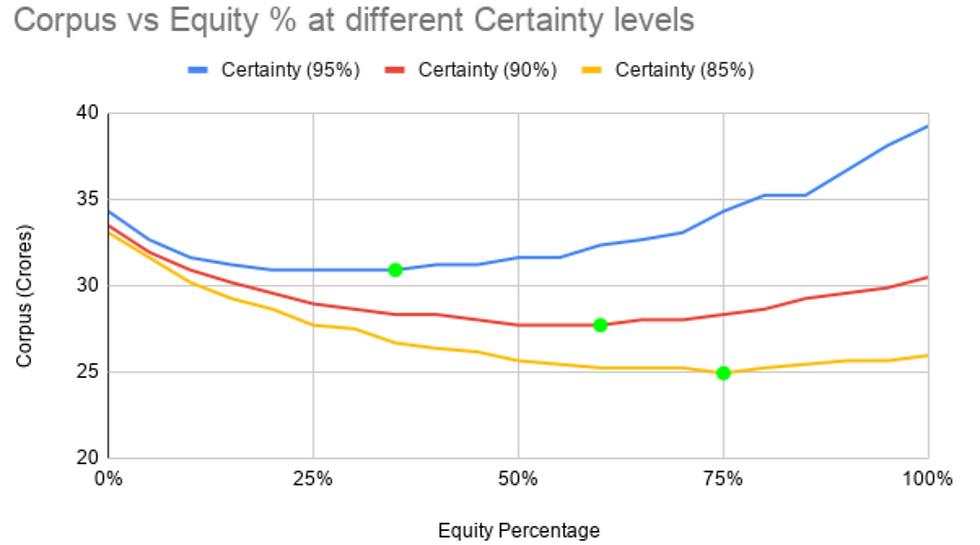

We’ll consider a simple portfolio between equity and debt in India. We have run millions of scenarios to generate the iso-certainty graphs below. Each line represents a corpus amount (y-axis) and asset allocation (x-axis) that meets the required success probability.

The minima at each isocertainty curve (green dots) give the minimum corpus and associated optimal equity allocation in the portfolio.

What does accepting lower uncertainty mean? They accept the risk that they have to adopt some dynamic spending - which is that they may forgo some discretionary expenses in the years markets don’t do well. There is a whole body of research here that we will discuss in later articles.

95% vs 85% Certainty Showdown

Metric | 95% Certainty | 85% Certainty |

Required Corpus | ~₹31 Crore | ~₹25 Crore |

Optimal Asset Allocation | 35% Equity : 65% Debt | 75% Equity : 25% Debt |

Median Legacy (at Age 90) | ~₹146 Crore | ~₹292 Crore |

The person choosing 85% certainty is freed from excessive pressure to save during their working years. It allows them to have a higher quality of life, more experiences when they are healthy. [Experiences are one of the top factors affecting happiness]

Somewhat counter intuitively, it also means that their portfolio by age 90 (their legacy) is higher. In reality, they will have a chance to spend more even in retirement than the person choosing 95% certainty!The higher median legacy under lower-certainty portfolios is primarily driven by higher equity exposure and greater long-term compounding in successful market outcomes.

The Legacy Paradox: Lower Certainty, Higher Wealth

The charts below show simulated wealth paths during retirement.

The solid blue line represents the median outcome, while the shaded bands show the range of outcomes across simulations (from pessimistic to optimistic scenarios).

Terminal Wealth Graph for 95% Certainty

Terminal Wealth Graph for 85% Certainty

Now, which one would you choose?

To be clear, this is not an argument for recklessness.

Sequence-of-returns risk is real.Longevity risk is real.Market crashes are real.

The goal of retirement planning is not to maximize risk-taking. It is to make intelligent tradeoffs between:

present quality of life,

retirement flexibility,

and long-term financial security.

The “right” answer will differ for every individual. The important thing is understanding the tradeoff clearly instead of blindly targeting the highest possible retirement corpus.

At Otto, we’ve built India-specific, tax-aware retirement models because we believe retirement planning in India deserves significantly more rigor than simplistic rules of thumb.

Future Discussion

There are several important questions that naturally follow from this discussion:(a) Are there better portfolios that reduce retirement burden(b) Why is corpus-equity curve convex (c) What dynamic spending strategies are useful etc. (d) Is the actual consumption geometric in practice?

We’ll look at these in part 2. Follow Otto for more such insights.

Disclaimer: This is not investment advice. Numbers are approximate and guidance from a proper investment advisor should be sought before making any decisions.

References:

Comments