Taxation

NSE IPO: The Dividend Trap

India's biggest cash machine is about to list. For a taxable investor, that dividend is a tax bill, not a reward. The largest corporate listing in India's history is on its way. In June, the National Stock Exchange (NSE) filed its DRHP for an OFS of ~₹30,000 crore. The number everyone repeats is the dividend. The NSE made a profit of ~₹10,300 crore in FY26. Zerodha's Nithin Kamath called it a "cash machine."

Here’s the catch. The rules don't let a stock exchange wander off into other businesses the way a normal company can. So the NSE makes a fortune, cannot reinvest it productively, and hands the cash (~84%) back to shareholders.

And that is exactly where the problem starts for a taxable investor. For most of our investors, applying for this IPO does not make much sense, and the reason has nothing to do with valuation. The thing everyone is celebrating is actually a drag due to double taxation.

There is a better way to own a business like this, and we will come to it. First, the trap.

An incorrect instinct

Ask most investors whether they would rather own a stock that pays a fat dividend or one that doesn't. Most pick the dividend. It feels like getting paid. It feels safe. A "cash machine" sounds like exactly what you want.

For a taxable investor in a high bracket, that instinct is backwards. Let’s see how.

Taxed once, then taxed again

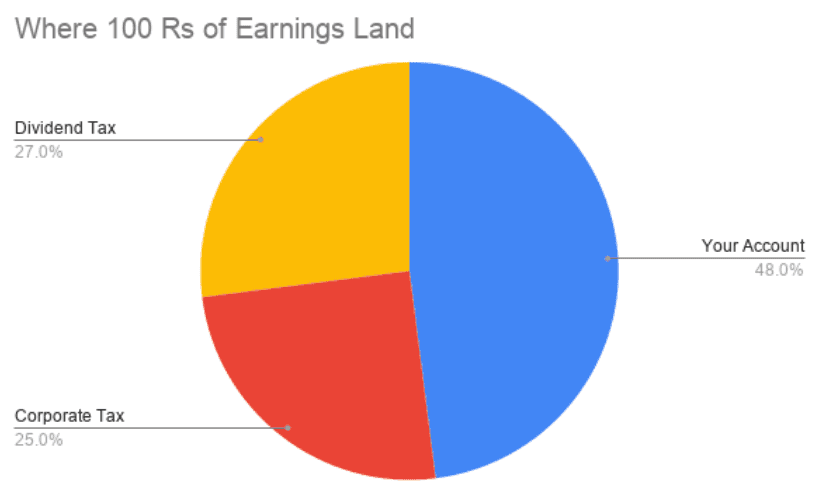

When a company earns ₹100 of profit, it first pays corporate tax. For most Indian companies that is roughly 25%. That is the first bite, and about ₹75 is left.

If the company hands that ₹75 to you as a dividend, it gets taxed again. This time it is taxed in your hands, at your personal slab rate.

Stack the two layers together. For a top-bracket investor, the dividend itself is taxed at about 36% (the 30% slab plus the capped surcharge and cess). Put that on top of the roughly 25% the company already paid, and about 52% of the original profit disappears between the company's books and your account.

That is the dividend trap. Under India's tax code, a company that pays you a large dividend is handing you a tax bill, not a gift.

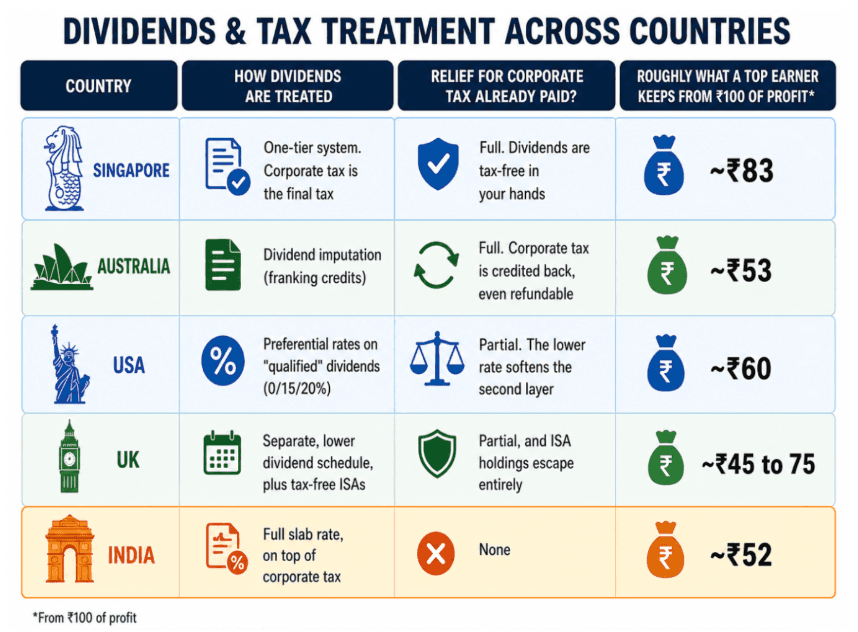

The rest of the world has already fixed it

Double taxation of dividends is not a uniquely Indian idea. It is the "classical" system many countries started with. The difference is that most of them did something about it. India did not.

*Illustrative, top-bracket investor, ₹100 of corporate profit distributed as a dividend. Real figures vary with income, surcharge and shelters.

Read that table the way a policymaker should. Singapore, Australia, USA, UK have softened the blow for investors. India taxes the dividend at full slab rates, with no relief for the corporate tax already paid. That is the harshest corner of the global table.

The valuation twist: a high dividend stock is worth less to you

At Otto, we care about post tax returns for investors. Our variation of DCF also runs with tax adjustments. We ran a discounted cash flow on the DRHP numbers. We have held back the valuation numbers due to regulatory constraints.

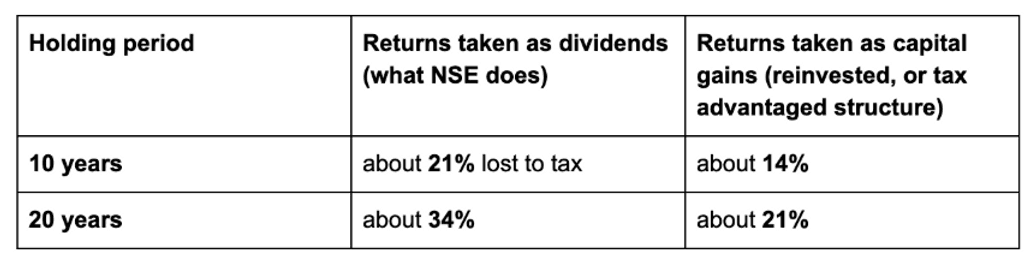

Because the NSE pays out around 84% of its profit every year, the bulk of what you collect while you hold the stock comes as dividends, taxed at about 36%, instead of being retained to compound into a capital gain you would be taxed about 15% on. It is that yearly dividend, not the eventual sale, that does the damage.

Here is how much of the business's value a top-bracket investor loses to personal tax, depending on how the returns reach them:

llustrative DCF on the DRHP figures, top-bracket investor. The figure is the share of pre-tax value lost to personal tax. The results are consistent across growth and discount-rate assumptions, because it is driven by the 84% payout and the gap between the ~36% dividend rate and the ~15% capital gains rate, not by the growth story.

Every year, the dividend is taxed at about 36%, while a capital gain would be taxed at about 15%. The longer you hold the cash machine, and the more it pays out, the more that gap compounds against you. It is a function of how the cash is returned, and how you choose to hold it. For most taxable investors, the answer to both points the same way, which brings us to the fix.

The workaround: mutual fund wrapper

An equity mutual fund does not pay tax on the dividends it receives from the companies it holds. Those dividends land inside the fund tax-free and compound in the NAV. You pay tax only when you redeem, and only at the long-term capital gains rate, about 15% for a top earner.

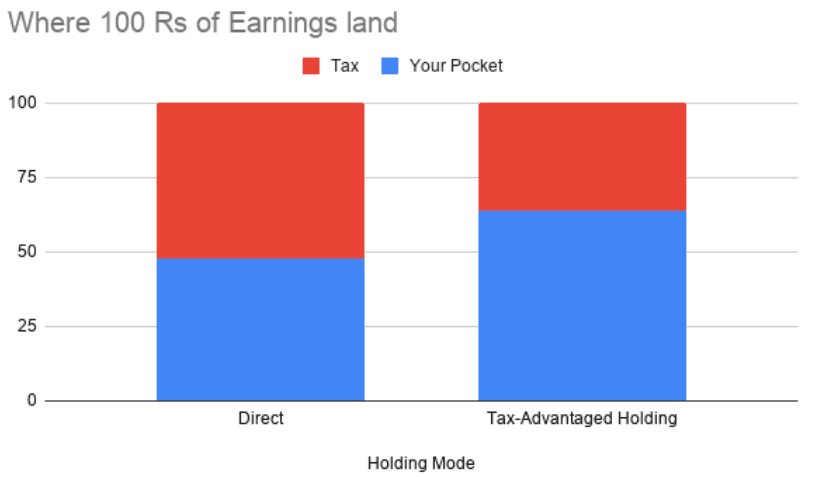

Put the two paths side by side for the same dividend-heavy company:

Hold it directly. Its dividends are taxed in your hands every year, at about 36%, on top of the corporate tax already paid.

Hold it inside an equity mutual fund. The dividends roll up untaxed within the fund. You pay about 15% only on the eventual gain, and only when you choose to sell.

This is not a loophole or a trick. It is simply how the law is written. For dividend-heavy businesses, the mutual fund stops being just a diversification tool. It becomes a legitimate tax wrapper that turns a doubly-taxed income stream into a lightly-taxed, deferred capital gain.

That brings us back to where we started. A high-payout business like the one about to list is not "good" or "bad" because of its dividend. But how you hold it changes your after-tax outcome a lot. For a long-term, taxable investor, the fund route can keep far more of every rupee the company earns.

Takeaway

Stop treating dividend yield as free money. For a high tax-bracket investor, a fat payout is often a tax liability dressed up as a reward. What builds wealth is total return, which is price appreciation plus dividends, measured after tax.

Mind the wrapper, not just the holding. The same company can be tax-efficient or tax-punishing depending on whether you own it directly or through a fund. For dividend-heavy names, the fund usually wins.

Remember that the code is not neutral. It nudges you, and the whole market, toward some structures and away from others. Usually nobody decided it should work that way. The investors who do best are not the ones who resent the taxman. They are the ones who understand the game he is quietly making everyone play.

This article is for educational purposes only and does not constitute investment, tax, or legal advice, or a recommendation to buy or sell any security, including the NSE. Tax rules are complex and depend on your individual circumstances, so please consult a qualified professional.

Disclaimer: Advice on Otto Money is provided by Wealth Beacon Investment Advisors (SEBI Reg. No. INA000020749). This is not investment advice - please consult a qualified Investment Advisor.