Gold

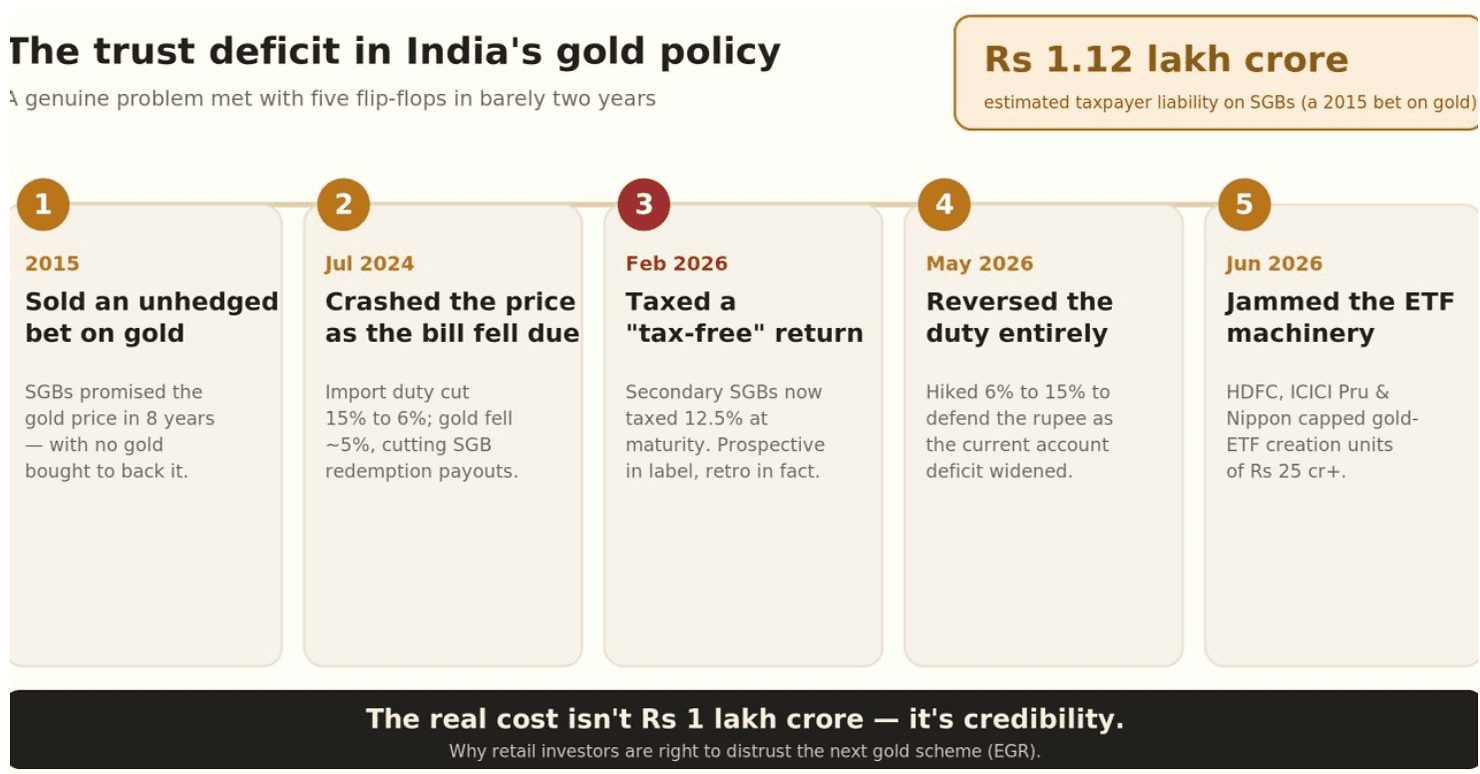

The trust deficit in India's gold policy

Indian taxpayers are now sitting on an estimated ₹1.12 lakh crore bill from a single bet the government placed on gold about a decade ago. That figure gets the headlines. What sits underneath it matters more. This is really a story about trust, and how a run of policy decisions has quietly taught retail investors to stop giving it.

To be fair, the underlying problem is real. Gold is India's second-largest import after crude oil. Every tonne that lands here drains dollars, widens the current account deficit, and weighs on the rupee, all for a metal that mostly ends up sitting in a locker. Nudging that demand into something more productive is a genuinely hard job, and we don't envy whoever has to do it.

So none of what follows is a quarrel with the goal. Our problem is with the execution. Over the past few years, policy on gold has jumped from one fix to the next, and along the way it has taught India's most patient savers a simple lesson: be careful what the government promises you about gold.

1. It started with an unhedged bet. In 2015, the government launched Sovereign Gold Bonds (SGBs). The pitch was clever. Instead of buying physical gold, you could hold paper that tracked the gold price, earned 2.5% interest a year, and paid out tax-free at maturity. Fewer imports, happier savers. But look at what the government actually did. It took your rupees today and promised to hand back the gold price eight years later, without buying a single gram of gold to cover that promise. That isn't a hedge. It's a naked short on gold, dressed up as a savings scheme. A bet like that only pays off if gold stays flat or falls. It did the opposite. Ten grams went from around ₹26,300 in 2015 to roughly ₹84,000 by early 2025, and the bill ballooned to an estimated ₹1.12 lakh crore. Even the government's own Economic Affairs Secretary eventually admitted SGBs had become a "high-cost method of borrowing." Fresh issuance quietly stopped after February 2024.

2. When the bill came due, the price conveniently fell. In the July 2024 Budget, the government cut the gold import duty from 15% to 6%. Gold dropped about 5% the same day. Investors redeeming their August 2016 bonds that month felt it directly, because their "tax-free" payout shrank right as a wave of redemptions was starting. Maybe that timing was a coincidence. It didn't look like one.

3. Then the tax deal changed under people's feet. Plenty of investors had bought SGBs on the secondary market, trusting the RBI's own printed promise that gains at maturity would be tax-free. Budget 2026 rewrote that. Now only the original subscriber keeps the exemption. Anyone who bought from someone else pays 12.5%, plus cess and surcharge, on redemption. The government insists this is "prospective from 1 April 2026." Tell that to someone who bought a bond in 2020 expecting a tax-free maturity in 2028 and is now being taxed on it. Prospective on paper, retrospective in real life.

4. Then the duty went straight back up. By May 2026, with the current account deficit widening and gold imports hitting a record $72 billion, the government reversed course again and pushed the duty from 6% back to 15%. So in under two years the same dial was spun from 15% to 6% and back to 15%, each time to put out whatever fire was burning loudest that quarter. Anyone trying to plan around it was left guessing.

5. And now the ETF plumbing is blocked. The duty hike made it expensive to source the gold that backs new ETF units. So in June 2026, HDFC, ICICI Prudential and Nippon India (Gold BeES) all capped fresh creation-unit subscriptions of ₹25 crore and above. That creation and redemption mechanism is the plumbing that keeps an ETF's market price anchored to the gold it actually holds. Choke it, and when demand spikes the ETF can float to a premium over its real value, with no easy way for anyone to arbitrage the gap shut. We have already seen this in the NASDAQ-100 ETFs - Gold ETFs could be next.

Take any one of these moves on its own and you can build a reasonable case for it. The imports, the deficit, the rupee, the redemption bill are all genuine pressures. But line them up and the pattern shows through. Each decision solved last quarter's emergency while quietly setting up the next one, and each was paid for partly in something that doesn't come back easily: the trust of people who took the government at its word. In just a few years, retail investors have watched the state write an unhedged bet and send taxpayers the bill, time a price crash to its own repayment calendar, tax a return it had called tax-free, flip an import duty 180 degrees, and clog the ETF machinery.

And there's always a next scheme. Electronic Gold Receipts (EGR) are being lined up as the future of formal, digitised gold in India. Their entire value rests on one fragile assumption: that the rules won't be quietly rewritten on you later. After everything above, who is going to believe that?

The problem India is trying to solve is real. But you don't fix a trust problem with policy that keeps proving you can't be trusted.

Disclaimer: Advice on Otto Money is provided by Wealth Beacon Investment Advisors (SEBI Reg. No. INA000020749). This is not investment advice - please consult a qualified Investment Advisor.

Sources: The Wire and Angel One (SGB liability); Upstox (2024 duty cut); Business Today and ClearTax (Budget 2026 SGB tax); CNBC and Business Standard (May 2026 duty hike); Business Today, Upstox and Outlook Money (June 2026 ETF restrictioIndian taxpayers are now sitting on an estimated ₹1.12 lakh crore bill from a single bet the government placed on gold about a decade ago. That figure gets the headlines. What sits underneath it matters more. This is really a story about trust, and how a run of policy decisions has quietly taught retail investors to stop giving it.